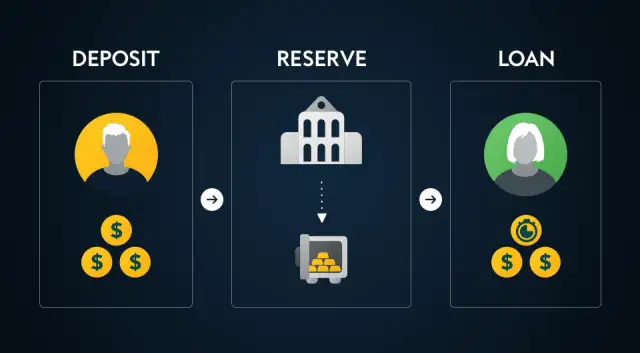

In fractional-reserve banking, the bank is only required to keep a portion of customer deposits on hand, freeing it up to lend out the remaining funds. This system is built to continuously increase the amount of money in the economy while keeping enough cash on hand to cover withdrawal requests.

Key Learnings

- A system known as fractional reserve banking enables banks to retain only a portion of customer deposits while lending out the remainder.

- Increased financial flow is made possible by this system.

- The system’s detractors claim that it increases the risk of a bank run, which would occur if there wasn’t enough money to cover withdrawal requests.

- The Federal Reserve is looking into the possibility of a central bank digital currency, which could alter banking as we currently know it.

Fractional-Reserve Banking: Definition and Example

In a fractional reserve banking system, banks use a portion of customer deposits as reserves and the remaining funds for loans to other clients. With the aid of this system, lending can be done with money that would otherwise be sitting in bank accounts, enabling consumers to keep borrowing and spending money, which boosts the economy.

Think about keeping $5,000 in your savings account as an illustration. Another client of the bank asks for a $1,000 loan. It may use a portion of all of the savings of one customer to help pay for another customer’s loan.

Note

If a nation has a central bank, it typically has the power to control the money supply and enact other policies to boost the economy. A requirement that banks maintain a certain amount in reserve to cover liabilities or unforeseen cash needs is one of the tools a central bank can use.

Functions of Fractional Reserve Banking

When banks utilize account balances while also making loans, the total amount of money in circulation increases. When you deposit money into your account, for instance, the bank displays 100% of it as being in your account, but it is permitted to lend some of it to other customers. Money in the economy is thereby increased as a result.

Imagine starting a brand-new economy and adding the initial $1,000 to it to demonstrate how it works.

1 – $1,000 is deposited into a bank account. The system has $1,000 right now.

2 – You choose to allow banks to lend 90% of their holdings. Afterward, the bank is able to lend its other clients $900.

3 – The system has $1,900 because those customers borrowed $900, and you still have $1,000 in your account.

4 – Borrowed funds are spent by customers, who then deposit the remaining $900 into their banks.

5 –The new $900 deposit can be financed by that bank to the tune of $810, or 90%.

6 – The $810 is lent by clients. The initial $900 recipients still have that money available in their accounts, and you still have $1,000 in your account. The system now has $2,710 ($1,000 + $900 + $810).

7 – The “money multiplier” cycle goes on forever.

Fractional-Reserve Banking is criticized

People typically don’t need access to all of their money at once, which makes fractional reserve banking practical. Even though your account might have $1,000 available, it’s unlikely that you’ll use it all at once. The reserves from other customer accounts should be enough to cover your withdrawal if you need to withdraw all of your money for some reason.

However, if everyone in the system makes a simultaneous withdrawal attempt, the system may fail. Customers frequently demand all of their cash from banks when they believe the institutions will fail, but banks do not keep enough cash on hand to meet this demand. Bank runs are what this is.

Because of fractional-reserve banking, bank failures during the Great Depression were disastrous—many people lost their entire life savings. As a result, the Federal Deposit Insurance Corporation (FDIC), which safeguards deposits in participating banks up to a certain amount, was established by the Banking Act of 1933.

In the event that a bank’s investments fail, the FDIC offers a government guarantee that customers will still receive their money. The National Credit Union Share Insurance Fund provides coverage comparable to this for credit unions.

Note

For these accounts, there is a $250,000 maximum insured amount. You would lose any funds over the insured amount if you had more in an account at a failed bank.

Fractional-reserve banking has drawn comparisons to a house of cards from critics. They are concerned that the economy could eventually implode and that there is nothing to support the system’s assets. Many worry that market participants will start to lose faith in the system.

Alternatives to fractional reserve banking

The Federal Reserve is looking into the possibility of a central bank digital currency, whose adoption could have a significant impact on the current fractional-reserve banking system.

A full-reserve banking system, in which banks maintain 100% of all deposits on hand at all times, is an alternative to a fractional-reserve system. This might apply to all deposits or just those made into accounts like checking and savings accounts that are meant to be used for quick cash needs. Less money will be available for lending if banks are forced to hold more cash in reserve, which will hinder economic expansion instead of helping it.

Your relationship with banks would be different without fractional-reserve banking. Banks may charge you for their services (or charge substantially more) than they would pay you in interest on your deposits. In the system we are accustomed to, banks make money by investing your funds and keeping the difference between the fees they charge borrowers and the interest they pay you, the depositor. A full-reserve system would have to devise a strategy to compete with this configuration.